The countdown to the beginning of the cycle of monetary easing in advanced economies, starting with the U.S., continues. Downbeat economic data or signs of lower consumer inflation improve market sentiment and investors place bets on more ambitious rate cuts happening earlier in the year, whereas reports in the opposite direction undermine asset prices. In the meantime, intriguing phenomena are occurring. For instance, the S&P 500 stock market index has returned a handsome 28% 12 months through February 29th but there is a twist. In the same period the return of a subindex comprising of the 10 largest listed companies, a sample heavily biased towards Information Technology (IT), was a jaw-dropping 60%. Therefore, everything else reduced overall performance by 32 percentage points.1

Stretching the time horizon a bit, it is possible to perceive other

compelling stories. Perhaps one of the most consequential of them relates to logistics. Although a substantial majority of these activities take place inside

economies, the fast globalization of the past few decades, even in its fractured, non-Western form of late, results in ever-increasing international operations. Foreign direct investment (FDI) flows related to transport, freight &

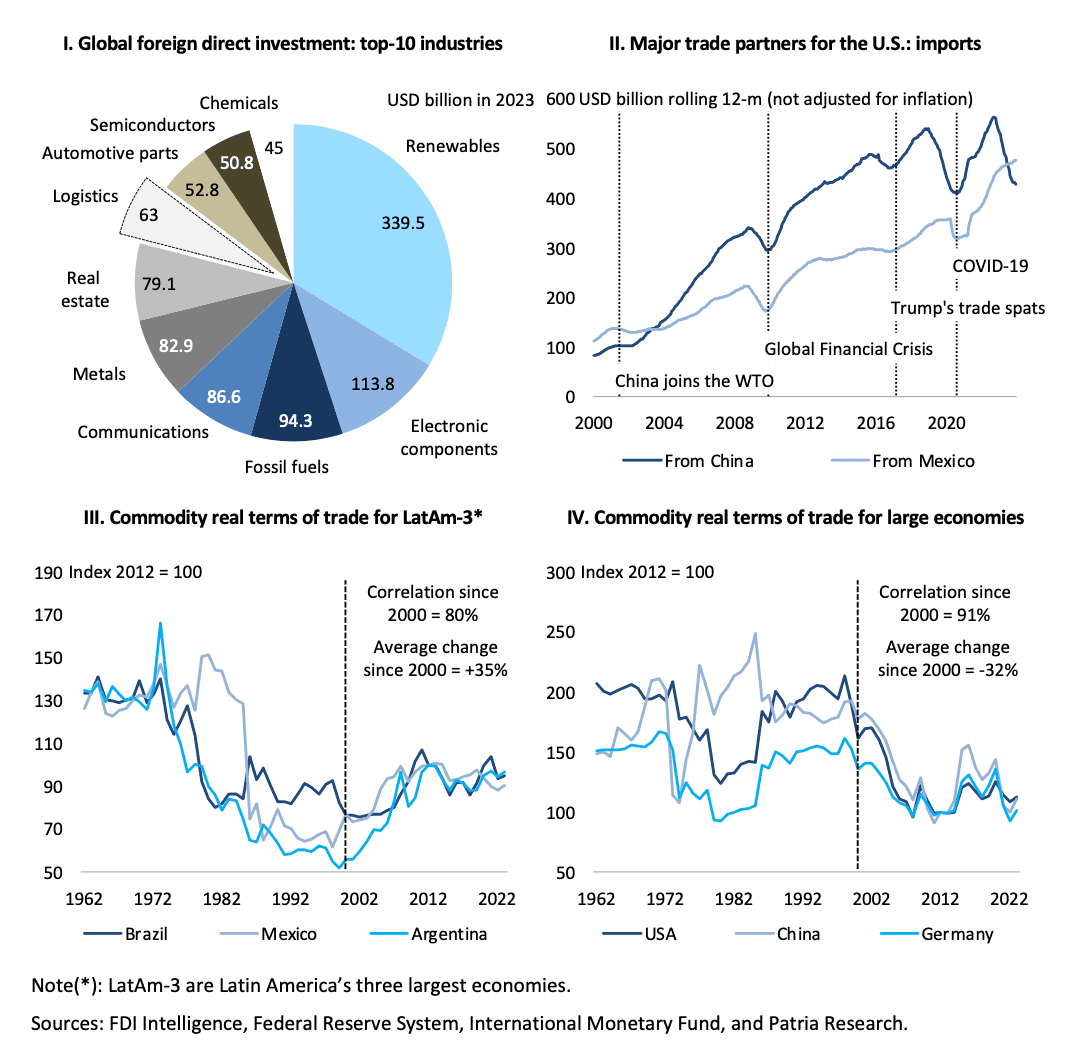

distribution, and warehousing & storage grew considerably. Indeed, they already rank among the Top-10 FDI globally, with USD63 billion recorded in 2023 (Chart I). Of course, the more the world experiences adverse shocks

such as weaponized economic relationships, severe geopolitical escalation and pandemic waves, the more strategic capital expenses to secure supply and value chains become. Thus, the clamorous ascent of re-shoring, friend-shoring and near-shoring strategies.

On that note, there are two other major global stories worth telling. The first, more complex, is the rearrangement of worldwide logistics to lessen the dependence of Western economies, notably those in Europe, on exports from Russia, especially oil & gas, minerals, and grains. Accordingly, there are novel networks of imports, storage and distribution emerging around the world. At the same time, however, another semi-clandestine system is shaping up with a focus on redirecting embargoed Russian goods to other markets. In this somewhat underground globalization scheme, large emerging nations such as India and China are playing a key role.

The second story is the steady transfer of value chains from China to U.S. allies, for example Taiwan and Mexico. In April 2022 the secretary of the Treasury Janet Yellen announced that America was intending to achieve free but secure trade by favoring the friend-shoring of supply chains to trusted nations. What then followed was something considerably more effective than President Trump’s ranting and ravings about unfair Chinese economic practices: Mexico is now the largest trading partner of the United States, reversing a trend of 20 years (Chart II). While China accounted for 14% of total U.S. imports in 2023, the smallest share since 2004, the decrease in some categories was even more

striking: Chinese information & communication technology (ICT) goods represented 45% of America’s ICT imports in 2018, but only 30% in 2023.2 To be sure, the world’s second largest economy should remain the global manufacturing base, as multinational companies are likely to shift to a “China plus one” or a “China plus many” strategy, maintaining some operations in the country to serve the local market, while adding facilities elsewhere. On the other hand, net foreign direct investment to Mexico recorded an all-time high of USD36 billion last year, 40% of which came from its big northern neighbor.

If the time horizon extends for half a century, there is an exceedingly interesting phenomenon associated to the Prebisch–Singer (PS) hypothesis. To recall, it argues that the price of primary commodities presents a downward secular trend relative to that of manufactured goods, thus causing the terms of trade of primary-product-based countries to deteriorate. For decades the PS thesis supported strategies of import-substitution industrialization (ISI) in developing nations. However, recent data strongly suggests a trend reversal. For Mexico, as well as for the largest Latin American economy - Brazil - and even for Argentina commodity prices deflated by manufactured goods’ unit values seem to follow a U-curve whose nadir was in the early 2000s (Chart III). After having decreased by 47% on average in real terms since the early 1960s, they rose by

35% on average since then, despite the diverse macroeconomic conditions in each geography. Not all primary products were created equal, though, and it makes quite a difference to have a competitive edge on animal proteins (beef, for instance) or energy products (oil & gas), whose terms of trade are trending up. Conversely, the performance of industrial minerals (sulfur and bauxite, for example), grains, or soft commodities, such as rubber and cotton, has been abysmal.3

But then the flip side of the trend under consideration is the deterioration in terms of trade for certain large economies (Chart IV). Among the most emblematic cases are the United States, a post-industrial society buoyed by a huge domestic market; China, a fast- growing emerging nation transitioning from an infrastructure-led development model; and Germany, an outstanding global exporter of manufactured goods. In spite of their different situations, they all have high level of technology

savvy but nevertheless face unfavorable shifts in relative prices that correlate highly since the turn of the century: average decline of 32%. The brave new world of artificial intelligence, blockchains, quantum computing and other revolutionary innovations still seems to have a special place for geographies that produce strategic primary products, after all.

1 Calculations on data from S&P Global https://www.spglobal.com/spdji/en/index- family/equity/us-equity/us-market-cap/#indices

2 Graham, N. and Rashid, M. (2023). “Is ‘friend-shoring really working?’. New Atlanticist, July 25th https://www.atlanticcouncil.org/blogs/new-atlanticist/is-friendshoring-really-working/.

3 Jacks, D. S. (2013). “From Boom to Bust: A Typology of Real Commodity Prices in the Long Run”. National Bureau of Economic Research, Working Paper 18874, March.

DISCLAIMER - Pátria Investimentos may have had, may currently hold, or may build up market positions in the securities or financial instruments mentioned in this research piece. Although information has been obtained from and is based upon sources Patria believes to be reliable, we do not guarantee its accuracy and it may be incomplete or condensed. All opinions and estimates constitute Patria 's judgment as of the date of the report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Any decision to purchase securities or instruments mentioned in this research must consider existing public information on such asset or registered prospectus. The securities and financial instruments possibly mentioned in this report may not be suitable for all investors, who must make their own investment decisions using their own independent advisors as they believe necessary and based upon their specific financial situations and objectives.